Form 1042-S Instructions

IRS Form 1042-S requires detailed reporting of U.S.-sourced income, withholding amounts, and recipient information. This guide provides step-by-step instructions for preparing and filing Form 1042-S.

Share this article

A Complete Solution to File IRS Form 1042 and 1042-S with TaxBandits

Download our FREE guide to stay

tax-compliant.

The guide includes:

- Overview of 1042 and 1042-S

- Step-by-Step Instructions

- How to File 1042-S Electronically

Related Articles

Related Blogs

IRS Form 1042-S Instructions

Updated on November 28, 2025 - 10:30 AM by Admin, TaxBandits

Withholding agents must file Form 1042-S to report U.S.-sourced income paid to foreign individuals and entities, including nonresident aliens and foreign corporations. This form ensures proper withholding and tax compliance for payments such as interest, dividends, and royalties.

Understanding Form 1042-S instructions helps prevent errors and ensures accurate reporting.

Line-by-Line Instructions to Fill Out Form 1042-S

Unique Form Identifier

First, as a withholding agent you must provide a unique form identifier number on each Form 1042-S.

The unique form identifier must:

- Be numeric (for example, 1234567891),

- Be exactly 10 digits, and

- Not be the recipient's U.S. TIN or FTIN.

When filing an amended Form 1042-S, the same unique form identifier must be used as the original to ensure proper correction. Each original Form 1042-S must have a unique identifier for the current year but can be reused in future years.

-

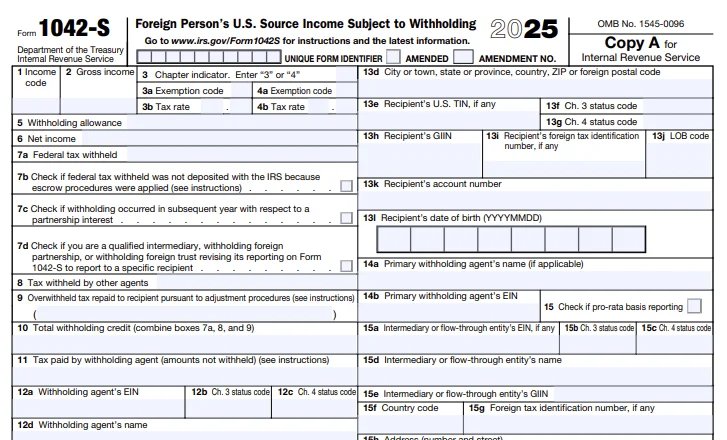

Box 1 - Income Code

Form 1042-S contains the income code, which identifies the type of income paid to the foreign recipient. The IRS assigns specific two-digit codes to different types of income. Here are the income codes:

Income Codes:

Interest Income Dividends Income 01 - Interest paid by U.S. obligors—general

06 - Dividends paid by U.S. corporations—general 02 - Interest paid on real property mortgages 07 - Dividends qualifying for direct dividend rate 03 - Interest paid to controlling foreign corporations 08 - Dividends paid by foreign corporations 04 - Interest paid by foreign corporations 34 - Substitute payment—dividends 05 - Interest on tax-free covenant bonds 40 - Other dividend equivalents under IRC section 871(m) 22 - Interest paid on deposit with a foreign branch of a domestic corporation or partnership 52 - Dividends paid on certain actively traded or publicly offered securities 29 - Deposit interest 53 - Substitute payments-dividends from certain actively traded or publicly offered securities 30 - Original issue discount (OID) 56 - Dividend equivalents under IRC section 871(m) as a result of applying the combined transaction rules 31 - Short-term OID 33 - Substitute payment—interest 51 - Interest paid on certain actively traded or publicly offered securities 54 - Substitute payments—interest from certain actively traded or publicly offered securities Other Income 09 - Capital gains

32 - Notional principal contract income 10 - Industrial royalties 35 - Substitute payment—other 11 - Motion picture or television copyright royalties 36 - Capital gains distributions 12 - Other royalties (e.g., copyright, software, broadcasting, endorsement payments) 37 - Return of capital 13 - Royalties paid on certain publicly offered securities 38 - Eligible deferred compensation items subject to IRC section 877A(d)(1) 14 - Real property income and natural resources royalties 39 - Distributions from a nongrantor trust subject to IRC section 877A(f)(1) 15 - Pensions, annuities, alimony, and/or insurance premiums 41 - Guarantee of indebtedness 16 - Scholarship or fellowship grants 42 - Earnings as an artist or athlete—no central withholding agreement 17 - Compensation for independent personal services 43 - Earnings as an artist or athlete—central withholding agreement 18 - Compensation for dependent personal services 44 - Specified federal procurement payments 19 - Compensation for teaching 50 - Income previously reported under escrow procedure 20 - Compensation during studying and training 55 - Taxable death benefits on life insurance contracts 23 - Other income 57 - Amount realized under IRC section 1446(f) 24 - Qualified investment entity (QIE) distributions of capital gains 58 - Publicly traded partnership distributions—undetermined 25 - Trust distributions subject to IRC section 1445 59 - Consent fees 26 - Unsevered growing crops and timber distributions by a trust subject to IRC section 1445 60 - Loan syndication fees 27 - Publicly traded partnership distributions subject to IRC section 1446(a) 61 - Settlement payments 28 - Gambling winnings -

Box 2 - Gross income

Enter the total amount paid to the recipient during the calendar year, including any tax withheld. Report the full payment amount even if part of it is non-taxable, subject to later determination, or withheld under escrow procedures.

Special rules apply for corporate distributions, contingent payments, notional principal contracts, and payments to artists or athletes under a central withholding agreement.

-

Box 3 - Chapter indicator

- For tax withheld under Chapter 3 (withholding on nonresident aliens), section 5000C, or backup withholding, the form should indicate Chapter 3.

- For tax withheld under Chapter 4 (FATCA withholding), Chapter 4 should be indicated.

-

Boxes 3 and 4 - Chapter 3 and Chapter 4 Exemption Codes & Tax Rates

If tax was withheld under Chapter 3 (withholding on nonresident aliens) or Chapter 4 (FATCA withholding), the applicable tax rate and exemption code must be reported. Only one option (either Chapter 3 or Chapter 4) can be chosen per form.

-

Exemption Codes (Boxes 3a and 4a)

If the tax rate in Box 3b or 4b is 00.00, an exemption code (01–24) may be required:

- Chapter 3 Exemptions (01–12, 23, 24) – Used for tax treaty benefits, U.S. tax law exemptions, and certain entity classifications.

- Chapter 4 Exemptions (13–21) – Applied when payments are exempt from FATCA withholding.

Rules for Completing Boxes 3a and 4a

- If tax was withheld under Chapter 4 (Box 4b > 0, not due to backup withholding), enter

“00” in Box 4a. - If tax was not withheld under Chapter 4 (Box 4b = 00.00), enter the applicable Chapter 4 exemption code (13–21) in Box 4a.

- If tax was withheld under Chapter 3 (Box 3b > 0, not due to backup withholding), enter “00”

in Box 3a. - If backup withholding applies, leave Box 3a blank.

Special Rule:

If exemption code 01 or 14 (effectively connected income) applies, the recipient’s U.S. TIN (Box 13e) must be provided. If unavailable, a 30% tax rate (30.00) must be applied, and “00” should be entered in

Boxes 3a and 4a. -

Tax Rates (Boxes 3b and 4b)

Enter the appropriate withholding tax rate based on Chapter 3 or Chapter 4 requirements:

- Chapter 4 (FATCA) withholding requires a 30.00% tax rate, unless an exemption applies.

- Chapter 3 withholding rates vary; refer to the Valid Tax Rate Table.

- Section 5000C (federal procurement payments) requires a 2% (02.00) tax rate, reported in Box 3b.

- If the payment is exempt from Chapter 4 withholding, enter 00.00 in Box 4b and include the exemption code in Box 4a.

- If different tax rates applied to the same type of income for a recipient, a separate Form 1042-S must be filed for each rate

Valid Tax Rate Table 00.00 10.00 24.00 02.00 12.00 25.00 04.00 12.50 27.50 04.90 14.00 28.00 04.95 15.00 30.00 05.00 17.50 37.00 07.00 20.00 08.00 21.00 -

Box 5 - Withholding allowance

Report the total amount exempt from withholding. This box should only be completed if you entered any of the following income codes in box 1:

- 16 - Scholarship or fellowship grants

- 17 - Compensation for independent personal services

- 18 - Compensation for dependent personal services

- 19 - Compensation for teaching

- 20 - Compensation during studying and training

- 42 - Earnings as an artist or athlete with no central withholding agreemen

This applies only when a valid tax treaty claim allows exemption up to a specific amount. Do not use this box to report a personal exemption. Also, if you are a designated withholding agent under a central withholding agreement, leave this box blank and report the full gross amount in Box 2.

-

Box 6 - Net Income

Report the net income in this box only if an amount is reported in box 5. If not, leave it blank.

-

Box 7a through 11 - Details About Federal tax withheld

Box 7a - Federal tax withheld

Enter the total amount of U.S. federal tax that you actually withheld in box 7a under Chapter 3 or 4. If no tax was withheld, enter "0" and do not leave it blank.

Box 7b - Federal tax withheld not deposited (Escrow Procedures Applied)

You can check this box if the federal taxes you withheld were not deposited with the IRS. Instead, you have followed escrow procedures.

If you used the escrow procedure, separate Forms 1042-S must be filed for those payments. Do not check this box if the payment was also subject to Chapter 3 withholding and tax was deposited under Chapter 3. Instead, select “3” in Box 3 and complete Box 3b.

What is the Escrow Procedure?

An escrow procedure is a legal concept in which a financial agreement, such as money, is held by a third party on behalf of the two other parties that are in the process of completing a transaction.

Box 7c - Withholding on foreign partner’s share after March 15

Check box 7c if you are a partnership that received an amount subject to withholding in the preceding year and you are withholding on the amount that belongs to a foreign partner’s share after March 15 of the subsequent year. You can check this box if withholding occurred in subsequent years with respect to a partnership interest.

Box 8 - Tax withheld by other agents

If you are a withholding agent filing a Form 1042-S to report income that has already been subject to withholding by another withholding agent, enter the amounts they withheld.

Box 9

This box should be completed only if you repaid a recipient under the reimbursement or set-off procedure during the 2027 calendar year. If you repaid the recipient under the reimbursement or set-off procedure during the 2026 calendar year, do not complete box 9. Instead, reduce the amount of withholding reported in box 7a.

Box 10 - Total withholding credit

Combine amounts reported in box 7a (Federal tax withheld), box 8 (Tax withheld by other agents), and box 9 (Overwithheld tax repaid to recipient pursuant to adjustment procedures).

Box 11 - Tax paid by withholding agent (amounts not withheld)

Enter the total amount of tax paid by the withholding agent from its own funds, rather than withholding it from the recipient’s payment. Do not include this amount in Box 10.

Also, this box should only be used when the withholding agent covered the tax liability directly, rather than deducting it from the payment to the recipient.

-

Boxes 12a to 12i -

Filing Agent Information

Box 12a - Withholding Agent's Employer Identification Number (EIN):

If you’re the withholding agent, you are required to enter your EIN. Suppose you are filing Form 1042 as a Qualified Intermediary (QI), Withholding Foreign Partnership (WP), or Withholding Foreign Trust (WT). In that case, you must enter your QI-EIN, WP-EIN, or WT-EIN.

Boxes 12b and 12c - Withholding Agent's Chapter 3 and Chapter 4 Status Code:

Enter the code(s) representing your withholding agent status. You'll find these codes in the Recipient Status Codes list in Appendix B. Remember to enter both a Chapter 3 and a Chapter 4 withholding agent status code, no matter what kind of payment you're dealing with.

If you're a U.S. financial institution (USFI), use the code 01 for your Chapter 4 status code unless a foreign branch of a USFI is filling out Form 1042-S – in that case, use the Chapter 4 code 50.

Boxes 12d - Enter Withholding Agent's Name.

Boxes 12e - Enter the Withholding agent’s Global Intermediary Identification Number (GIIN).

Boxes 12f - Country code

Enter your country code from the IRS list of foreign countries. If you can’t locate the code for the country in the list, enter ‘OC.’

Box 12g to 12i - Foreign Tax Identification Number

Enter the Foreign Tax Identification Number (if any) and address details of the withholding agent.

-

Boxes 13a Through 13d -

Recipient's Name, Country Code, and Address

Box 13a - Recipient’s Name

Enter the recipient’s full legal name. If the name is unknown, enter “Unknown Recipient.” For withholding rate pools, use “Withholding Rate Pool” (Chapter 3) or a Chapter 4 pool description (e.g., “Nonparticipating FFI Pool”). Only one joint owner should be listed.

If the recipient is a QI acting as a QDD, use the name from Form W-8IMY, including branch identifiers

if applicable.Box 13b - Recipient’s Country Code

Enter the two-letter country code of the recipient’s tax residence. Use “OC” for unknown recipients or “US” for

U.S. persons.Boxes 13c & 13d – Recipient’s Address

Provide the permanent address (no P.O. Boxes unless required). For FFIs or QIs reporting a withholding pool, use the FFI/QI’s address.

-

Box 13e and 13h

- Recipient’s U.S. TIN and GIIN

A U.S. Taxpayer Identification Number (TIN) is required if the recipient meets any of the following conditions:

- Has effectively connected income (ECI) from a U.S. trade or business (enter Exemption Code 01 in Box 3a or 14 in Box 4a).

- Claims a reduced tax rate or exemption under a tax treaty but does not provide a Foreign Tax Identification Number (FTIN) (Box 13i), unless the income is an unexpected payment or involves actively traded investments like stocks, debt obligations, or certain mutual funds.

- Is a nonresident alien seeking a tax exemption under section 871(f) for annuities from

qualified plans. - Is a foreign organization claiming tax-exempt status under section 501(c) or as a

private foundation. - Is a Qualified Intermediary (QI) that does not disclose recipient details (not acting as the recipient).

- Is a Withholding Foreign Partnership (WP) or Withholding Foreign Trust (WT).

- Is a nonresident alien individual claiming an exemption from withholding on independent

personal services. - Is a U.S. branch of a Foreign Financial Institution (FFI) or a Territory Financial Institution treated as a U.S. person.

- Is a Qualified Securities Lender (QSL) receiving substitute dividend payments.

- If a recipient voluntarily provides a U.S. TIN on Form W-8, it must still be reported. A U.S. TIN is also required if the recipient uses Form 1042-S to claim a tax refund or credit.

A Global Intermediary Identification Number (GIIN) is required if Chapter 4 documentation mandates it. If the payment is made to a disregarded entity or branch listed in Part II of Form W-8BEN-E, enter the GIIN of the disregarded entity or branch.

-

Boxes 13f and 13g

- Recipient’s Chapter 3 and Chapter 4 Status Codes

Enter the recipient status code from the list of Recipient Status Codes in Appendix B. There are special instructions for applying for the status codes in Chapters 3 and 4. To learn more about them, click here.

You need a Chapter 4 status code only if the payment falls under withholdable payment or when a participating FFI or registered deemed-compliant FFI gives a Chapter 4 withholding rate pool of U.S. payees.

The Chapter 4 status code may be determined under the applicable IGA by a withholding agent that is an FFI subject to such an agreement.

-

Box 13j

- LOB Code

Enter the code that best describes the applicable limitation on benefits (LOB) category that qualifies the taxpayer for the requested treaty benefits.

-

LOB Code

- LOB Treaty Category:

- 02 - Government – contracting state/political subdivision/local authority

- 03- Tax-exempt pension trust/Pension fund

- 04 - Tax-exempt/Charitable organization

- 05 - Publicly traded corporation

- 06 - Subsidiary of publicly traded corporation

- 07 - Company that meets the ownership and base erosion test

- 08 - Company that meets the derivative benefits test

- 09 - Company with an item of income that meets the active trade or business test

- 10 - Discretionary determination

- 11 - Other

- 12 - No LOB article in treaty

-

Box 13k

- Recipient’s Date of Birth

Use box 13l to enter the recipient’s date of birth. The correct format is YYYYMMDD (for example, enter “20001205” for a date of birth of December 5, 2000).

-

Box 13l

- Recipient Account Number

If you are a financial institution reporting payments paid to a direct account holder for an account held by you at your U.S. office or branch, you must provide the recipient's account number in box 13k.

If the payment is made through a (nonqualified intermediary) or flow-through entity, you are not required to use this box.

-

Box 14a and 14b

- Primary Withholding Agent's Name and EIN

Suppose you're an intermediary or a flow-through entity who reports amounts withheld by another withholding agent. In that case, provide the name and EIN of the primary withholding agent that withheld the tax.

-

Box 15

- Pro-Rata Basis Reporting Checkbox

You must check box 15 to notify the IRS that the NQI (nonqualified intermediary) used the alternative procedures of regulations section 1.1441-1(e)(3)(iv)(D) failed to comply with those procedures.

-

Boxes 15a through 15i

- Intermediary/ Flow Through Entity's Name, Status Code, Country Code, Address, EIN, GIIN, and Foreign Tax Identification Number

Box 15a to 15e

Enter the Intermediary or flow-through entity EIN(if any), Chapter 3 or 4 status code, name, and GIIN.

Box 15f - Country code

Enter the country code for the country where the intermediate or flow-through entity is located.

Box 15g - Intermediary or flow-through entity's FTIN

In box 15g, enter the tax identification number of the intermediate or flow-through entity used in the country of residence for tax purposes. Please note Box 15g is optional.

Box 15h and 15i

Enter the Intermediary/ Flow-Through Entity's address, city or town, state or province, country, ZIP, or foreign postal code.

-

Box 16a to 16e

- Payer's Name, TIN, GIIN, and Status Code

If the person giving you the amount (payer) has a different name, TIN, or GIIN (Global Intermediary Identification Number) compared to the withholding agent mentioned in boxes 12a, 12d, and 12e, be sure to include the

correct details.If the payment is managed by a transfer agent or a paying agent who is also handling withholding on behalf of the payer, enter the status codes for both Chapter 3 and Chapter 4 that apply to the payer in boxes 16d and 16e.

-

Boxes 17a Through 17c

- State Income Tax Withheld and Related Information

Include in these boxes information relating to any state income tax withheld.

Which Copies of Form 1042-S Need to be Submitted?

The Form 1042-S contains four copies, and the recipient receives 3 out of them. The different copies of Form 1042-S are:

- Copy A is for use by the IRS.

- Copy B is for the recipient.

- Copy C is for the recipient, must be attached to any federal tax return filed.

- Copy D is for the recipient, must be attached to any state tax return filed.

When is the Deadline for Reporting 1042-S?

Generally, the due date for filing Form 1042-S with the IRS is March 15th of the calendar year in which the income was paid. If March 15th falls on a weekend or legal holiday, the due date is the next business day.

Click here to know the due date to file Form 1042-S for the 2025 tax year.

How to Submit Form 1042-S?

To file Form 1042-S, complete all applicable sections based on the type of income and withholding applicable. The IRS accepts Form 1042-S filings both on paper and online. However, the IRS requires e-filing Form 1042-S for withholding agents filing 10 or more information returns annually or for partnerships with over 100 partners, as per the latest IRS revisions to Form 1042. Choose TaxBandits to meet your 1042-S filing deadline to ensure compliance.

TaxBandits, an IRS-authorized e-file provider, allows you to e-file Form 1042-S with the IRS and receive instant status updates on your Form 1042-S returns. Get to know how TaxBandits simplifies your 1042-S filing process!

Helpful 1042-S Resources

Success Starts With TaxBandits

An IRS Authorized E-file provider you can trust